Near term Optimize, then long term boulders in the stream ahead for Netflix.

| Investment Recommendation |

| Our recommendation is a Sell for NFLX in the near term as it current price for investors to take their earnings now before current headwinds potentially negatively impact the stock price. The past performance is the company shows good potential for long term stable growth and would watch for buying opportunities if stock moves closer to its value target below. |

- Valuation of business estimated to be $77.9B

- We believe NFLX currently has more downside risk than upside potential at its current market price and long term outlook.

Current Price: $361.21 / share

Revenue Growth

Operating Margin

Return on Capital

Reinvestment % EBIT(1-t)

Value Target: $124.00 / share

3.0%

14.86%

8.74%

34%

| Recommendation Drivers |

Netflix is currently in a strategic shift, moving from the premier streaming content platform into a fragmented content creation and distribution. Netflix is currently in a leader position of streaming services in the United States and Europe. We see this strong position to yield excess returns in the near term but will be a challenge longer term. They seek to rapidly expand internationally launching in ~130 countries (with a focus on India), however thus far that growth has struggled.

Consolidation of premium entertainment studios. Recently there have been a flurry of large acquisitions like AT&T’s of Time Warner, Disney of Fox production assets and other smaller mergers. Content control is being consolidated into larger portfolios increasing content acquisition costs or complete inability of Netflix to get access to premium titles.

In house content creation expensive and risky. Netflix spent $8B on original content in 2018, increasing by $1B / year for the past several years with the trend to continue. Their current bottom up beta is 1.28, comprised of over 30 companies with a blend of technology and entertainment companies. We expect 1.3-1.4 moving forward, more in line to entertainment average (1.63) but not completely as distribution platform and user preference data gives them insights to manage the business better. Content creation introduces risk going into direct competition with the likes of Disney who excel at managing content franchises and were previously a content provider to Netflix. This can already be seen with Disney dissolving the agreement enabling Netflix to create new season of their popular Marvel super hero series. Netflix will need new franchises to capture audiences’ customers, shifting outside their core competency, exposing them to new risks with simultaneously higher capital demands.

Market Price vs. Business Valuation

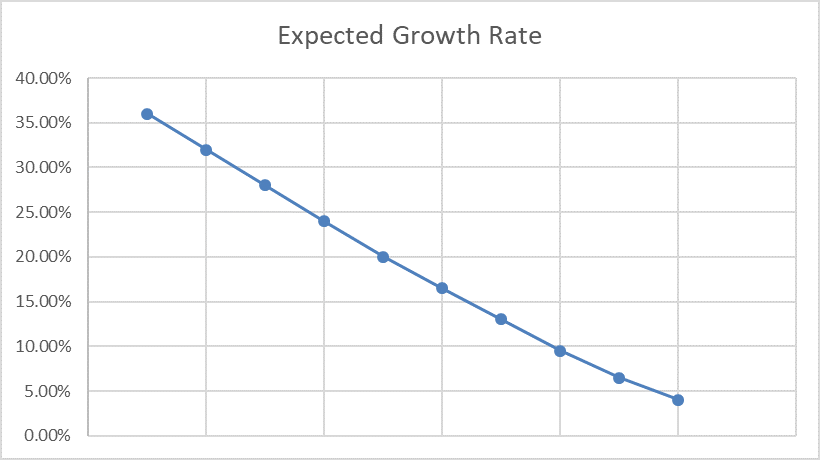

Current market price frames Netflix as a high growth technology company. As they shift to a hybrid business of entertainment creation and streaming platform their expectations should be in line with this business strategy reflecting the new inclusion of entertainment industry risks. At its current price the market appears to be expecting over 5% growth indefinitely. We expect their high growth period to be in decline from its current high with a 18% CAGR over the next 10 years then decelerating to 3% growth rate in perpetuity.

Value of Operating Assets

+ Cash & Non-Op

= Value of Frim

– Value of Debt

= Value of Equity

– Equity Options

Value per Share

$50,442

$27,543

$77,984

$22,283

$55,701

$1,601

$124

Sensitivity Analysis

- Assumed ROC = CoC. If ROC = 14%, Reinvestment Rate & weight of debt decreases adding ~$11B to the firm’s value.

- Assumed CAGR for 10 years = 18.5, adjusting to 40% rate increases the firm’s value to $193B ($389 per share).

- Assumed Beta remains 1.3, increasing Beta to 1.8 decreases value to $65B ($95 per share). Decreasing Beta to 0.9 increases value to $95B ($161 per share).

- Assuming an industry avg. operating margin, adjusting the operating margin from 15% to 20% increases the value of the firm to $107B ($190 per share)

Damodaran Online is a recommended resource for doing similar equity valuations. Pre-built spreadsheet models can be found in the Tools -> Spreadsheets -> Valuation.

Update August 2020: This was an equities valuation practice based on their current market position and forward looking revenue and cash growth. We estimated that Netflix would show stable growth but then struggle for growing in an increasing competitive market of direct streaming entertainment. This valuation was created before the world events of COVID-19. We did not consider any “black swan” world event which Netflix has been uniquely positioned to grow. This demonstrates how valuations are inherently just a snapshot with the known information at the time and will need to be reconsider over time with change.

NFLX dropped to a low of $263.03 on Sept 27, 2019. Before hitting an all time high of $548.73 on July 10, 2020 and currently still trades above $500 in early August of 2020.

Recent Comments